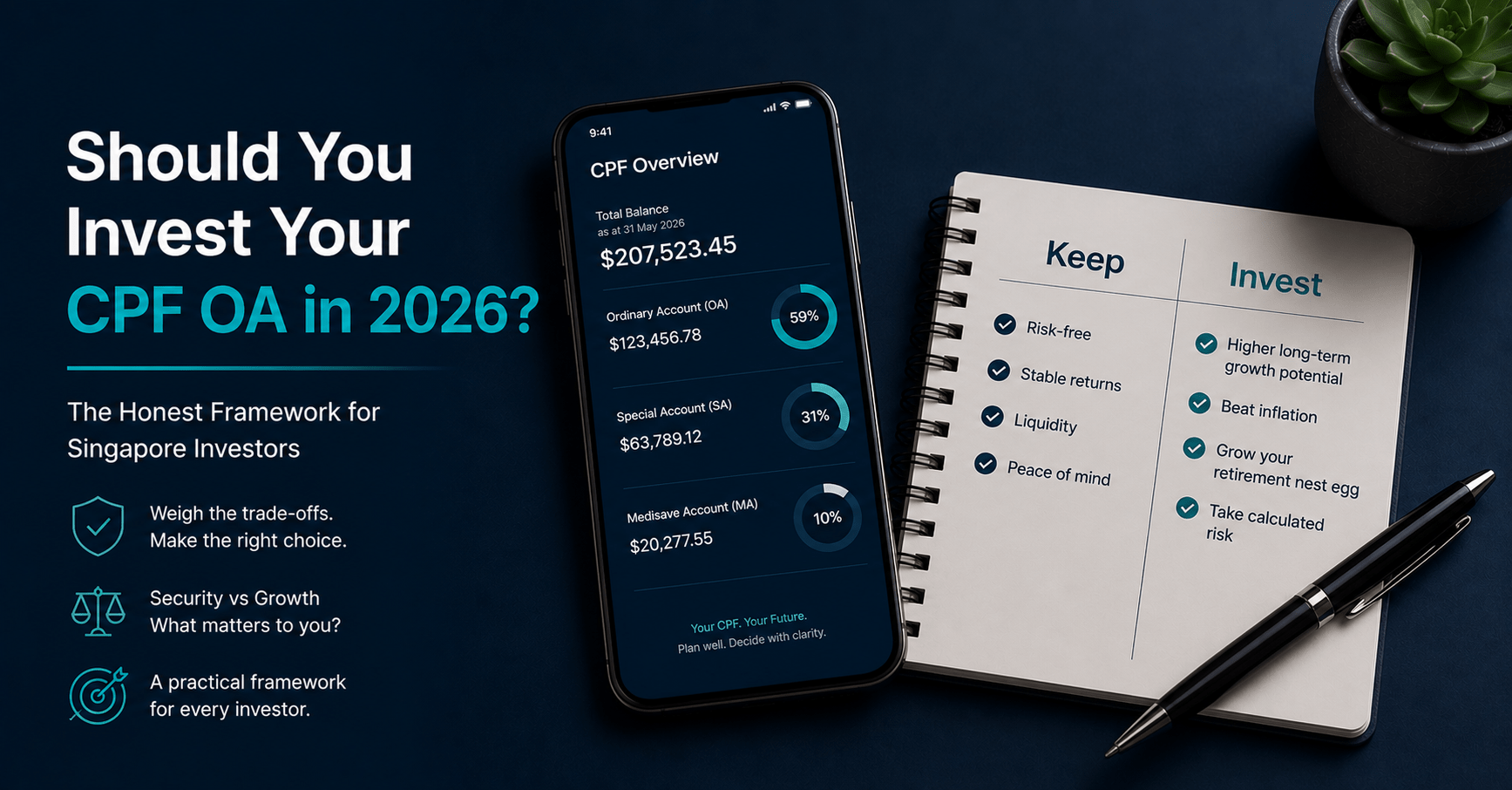

Should You Invest Your CPF OA in 2026? The Honest Framework for Singapore Investors

Table of Contents

A note before we begin: The content on DLCuration is produced for general informational purposes only. It does not take into account your individual financial situation, goals, or needs. Nothing published here constitutes financial, investment, or trading advice — and it should not be treated as such. CPF rules, interest rates, and scheme details are subject to change — always verify the latest information on the official CPF Board website at cpf.gov.sg before making any decision. While we make every effort to ensure accuracy, DLCuration makes no representation and accepts no liability for any losses that may arise from decisions made based on this content. If you are unsure about any CPF-related financial decision, please consult a licensed financial adviser.

The CPF OA investing question is the most reliably polarising topic in Singapore personal finance.

One camp says leaving money in CPF OA at 2.5% p.a. is sub-optimal — inflation erodes purchasing power, markets historically return more, and the same portfolio construction you would use for cash savings applies to CPF money too. The other camp says CPF OA is not just another savings account — it is the foundation of your housing plan, your retirement safety net, and a guaranteed risk-free return that most investment portfolios will fail to beat consistently after costs and behavioural mistakes.

Both positions contain truth. Neither is complete. The decision to invest or keep your CPF OA is genuinely personal — it depends on your age, housing plans, existing investment portfolio, risk tolerance, and how long you have until retirement. There is no universal right answer.

What there is: a framework for making the decision rigorously rather than emotionally, and a clear map of the conditions under which investing makes sense versus when leaving your money in CPF OA is genuinely the better call.

This article walks through both, using current 2026 rates and rules.

Reminder: CPF rules change. All figures and eligibility criteria in this article reflect CPF Board announcements current as of May 2026. Verify at cpf.gov.sg before making any decision. Nothing here constitutes financial or investment advice.

First: Understand What You Are Actually Deciding

The CPF OA investing decision is not simply “2.5% guaranteed vs. potentially more in the stock market.” That framing is too narrow. Here is what the decision actually involves:

1. You are deciding to exchange a guaranteed return for a variable one. The CPF OA’s 2.5% p.a. is not a promotional rate, not a bank’s discretionary rate, and not dependent on any conditions you must meet. It is legislated, government-backed, and guaranteed. The 4% floor rate on your SA, MA, and RA — extended until 31 December 2026 — follows the same logic. No investment product offers that combination of certainty and accessibility.

2. Any gains stay in CPF. This is a point many people gloss over. If you invest your CPF OA and your portfolio gains 10%, that 10% goes back into your CPF account — not into your pocket. You cannot withdraw investment profits unless you have set aside the Full Retirement Sum in your Retirement Account. CPF investing is not a route to a cash payout. It is a tool to potentially reach retirement with a larger CPF balance.

3. If you lose money, you do not have to top up CPF — but you have less. Losses from CPFIS-OA investments are absorbed by you. CPF Board does not make up the shortfall. A loss on your CPFIS investment means arriving at retirement with less in your OA than you would have had by leaving the money untouched and earning 2.5% p.a.

4. Your CPF OA has multiple roles. If you are buying an HDB flat, servicing a mortgage, or planning to do either in the next one to three years, your CPF OA is not purely an investment account — it is your housing down payment buffer and loan repayment source. Investing that money introduces timing risk: what happens if your portfolio is down 20% the month you need the funds for your housing transaction?

Keep these four realities in mind throughout the framework below.

The Current CPF Interest Rate Picture (2026)

The Ordinary Account interest rate remains unchanged at the floor rate of 2.5% per annum from 1 April to 30 June 2026, as the OA pegged rate remains below the floor rate of 2.5%.

The Special, MediSave and Retirement Accounts interest rate remains unchanged at the floor rate of 4% per annum from 1 April to 30 June 2026.

To help boost retirement savings, the government pays extra interest on the first S$60,000 of your combined balances, capped at S$20,000 for the Ordinary Account. The extra interest earned on OA savings goes into your Special Account or Retirement Account.

In practice, this means the effective return on your first S$20,000 of OA savings is 3.5% p.a. (2.5% base + 1% extra interest) — though that extra 1% is credited to your SA, not your OA. For balances above S$20,000 in OA, the rate is the standard 2.5% p.a.

Here is the full current rate picture:

| Account | Base Rate | Extra Interest (first S$60k combined, capped) | Effective Rate |

|---|---|---|---|

| Ordinary Account (OA) | 2.5% p.a. | +1% on first S$20,000 (credited to SA/RA) | 2.5% in OA; 3.5% effective on first S$20k |

| Special Account (SA) | 4.0% p.a. | +1% on remaining combined balance up to S$60k | Up to 5% effective |

| MediSave Account (MA) | 4.0% p.a. | Included in combined balance cap | Up to 5% effective |

| Retirement Account (RA) | 4.0% p.a. | +2% extra on first S$30k for members 55+ | Up to 6% effective for seniors |

The headline: leaving money in CPF — particularly in your SA — earns meaningfully more than most Singapore savings accounts in 2026, and does so with zero risk and zero conditions.

How CPF OA Investing Actually Works (CPFIS-OA)

Before deciding whether to invest, you need to understand the mechanics clearly.

What CPFIS-OA is

The CPF Investment Scheme – Ordinary Account (CPFIS-OA) allows you to invest your CPF OA savings in approved financial products — potentially earning more than the default 2.5% p.a. return. The scheme lets you invest your CPF savings in different products with varying risks and returns. You can also leave your CPF savings in your accounts to grow steadily with stable, risk-free interest.

What you can invest in

Under CPFIS-OA, approved products include:

- Unit trusts — managed funds, the most commonly used CPFIS product

- Exchange Traded Funds (ETFs) — including index ETFs like the Nikko AM STI ETF

- SGX-listed stocks — subject to the 35% stock limit

- Government bonds and T-bills

- Fixed deposits with approved banks

- Investment-linked products (ILPs) from approved insurers

- Gold — up to 10% of investible savings

The minimum balance rule

You can invest your OA savings after setting aside S$20,000 in your OA. Additionally, you can only invest up to 35% and 10% of your investible savings in stocks and gold respectively.

This means: if your OA balance is S$30,000, only S$10,000 is investible. If it is S$50,000, S$30,000 is investible. The first S$20,000 must remain in your OA at all times.

Investible savings calculation:

Investible savings = OA balance + CPF withdrawn for investment and education — S$20,000 minimum buffer

How to set it up

- Complete the CPFIS Self-Awareness Questionnaire (SAQ) — mandatory for new investors since October 2018, completed online via the CPF website

- Open a CPF Investment Account (CPFIA) with one of the three agent banks: DBS/POSB, OCBC, or UOB

- Open a brokerage account if investing in ETFs or stocks — the brokerage must be CPFIS-approved (DBS Vickers, OCBC Securities, UOB Kay Hian, and others qualify; IBKR, Webull, and Longbridge do not)

- Transfer CPF OA funds into your CPFIA and execute your investment from there

Important: All gains from CPFIS-OA investments return to your CPF account — not to your bank account. You cannot access profits as cash unless you meet the Full Retirement Sum withdrawal conditions.

The Decision Framework: 5 Questions to Answer Before Investing

Work through these five questions in order. Your answers determine whether investing your CPF OA makes sense for your specific situation.

Question 1: Do you need this money for housing in the next 3 years?

If yes → keep it in CPF OA.

If you are planning to buy an HDB flat, top up your home loan, or fund a renovation with CPF OA in the next one to three years, that money is not long-term investment capital — it is near-term liquidity with a specific purpose. Investing it introduces the risk that markets decline at exactly the wrong time. A 20% market drawdown in the 12 months before your BTO reaches completion means either selling at a loss or finding cash to cover the gap.

CPF OA money earmarked for housing should stay in CPF OA, full stop.

Question 2: Have you already maximised your SA?

If no → consider transferring OA to SA before investing.

The CPF SA earns 4% p.a., and the government extended this floor rate until 31 December 2026. If you have OA money you are not planning to use for housing, and your SA has not reached the Full Retirement Sum, transferring OA funds to SA earns you a guaranteed 4% p.a. — 1.5 percentage points more than leaving it in OA and 60% more than any investment would need to return to justify the switch.

Critical caveat: OA to SA transfers are irreversible. Once transferred, the money cannot return to OA. It cannot be used for housing. It cannot be invested in CPFIS-OA. It is locked in SA until retirement. If housing flexibility matters to you — even theoretically — think carefully before transferring.

Also note: a major change for 2026 is the full implementation of the SA closure for seniors. When you turn 55, your SA is closed and SA savings are transferred to your RA up to your FRS. Any remaining balance goes to your OA. This means the SA shielding strategy used by some investors is no longer available after age 55. The OA-to-SA transfer is most powerful for investors in their 30s and early 40s with a long runway for the 4% to compound.

Question 3: Can your investments realistically beat 2.5% p.a. after all costs?

This is the core maths question — and it is trickier than it looks.

The hurdle rate is not just 2.5%. Once you account for the all-in cost of investing, the true hurdle is higher:

| Cost Component | Typical Amount |

|---|---|

| CPFIS-OA agent bank fee (DBS, OCBC, UOB) | S$2.00–S$2.50 + 9% GST per transaction |

| Fund management fee (if using unit trusts) | 0.30–1.50% p.a. |

| ETF expense ratio (if using index ETFs) | 0.15–0.50% p.a. |

| Brokerage commission (if buying stocks/ETFs directly) | 0.08–0.25% per trade |

| Effective hurdle rate | Approximately 2.5% + 0.30–1.50%+ p.a. depending on products chosen |

Using actively managed unit trusts with a 1.0% management fee means you need your underlying investments to return approximately 3.5–4.0% p.a. just to match leaving your money in CPF OA — not to beat it.

Index ETFs via CPFIS reduce this gap significantly. The Nikko AM STI ETF has an expense ratio of approximately 0.30% p.a. — meaning the hurdle rate for an STI ETF investment is approximately 2.8%. If the STI consistently returns more than 2.8% p.a. over your investment horizon, the investment is additive. In many historical periods it has; in others it has not.

For low-cost ETF investing through CPFIS, the break-even is achievable. For high-fee actively managed funds, it is not — and this is precisely why the CPFIS product list has been tightened over the years to remove high-cost funds.

Question 4: What is your investment time horizon?

The shorter your horizon, the less compelling the case for investing.

Equity markets deliver higher returns than 2.5% p.a. over long time horizons — decades, not years. Over shorter horizons (five years or fewer), the probability of underperforming the CPF OA’s guaranteed return increases meaningfully. A market correction of 20–30% in year three of a five-year investment window may not recover before you need the money.

General rule of thumb:

- Under 40, no near-term housing plans, more than 10 years to retirement: the case for investing CPF OA in a low-cost, globally diversified ETF is reasonable

- Over 50, or within 5 years of needing the funds for any purpose: the guaranteed 2.5% p.a. becomes increasingly hard to beat on a risk-adjusted basis

- Between 40–50: the decision depends primarily on your housing situation and existing investment portfolio — there is no universal answer

Question 5: Do you already have a separate cash investment portfolio?

If yes, the urgency to invest CPF OA diminishes.

If you are already investing 15–20% of your monthly salary in a globally diversified ETF portfolio via Webull, Longbridge, or IBKR, you already have equity market exposure and are benefiting from long-term compounding in a format where you can actually access gains in cash. Adding CPF OA to your investment pool provides additional equity exposure — but at the cost of liquidity and with gains that remain locked in CPF.

For investors who have not started their cash investment portfolio yet, the priority is almost always to build that first. The flexibility of cash investments — accessible, redeployable, genuinely yours in cash terms — is worth more at an early stage than the incremental return from also investing your CPF OA.

The Verdict: Who Should Invest Their CPF OA in 2026

You should seriously consider investing your CPF OA if:

- You are under 40, with no housing plans in the next three years

- Your OA balance is above S$20,000 (so you have investible savings above the buffer requirement)

- You choose low-cost index ETFs or funds with a combined expense ratio below 0.50% p.a.

- You have a cash investment portfolio already running — you understand market volatility and will not panic-sell during a correction

- You invest for a minimum 10-year horizon and are comfortable leaving the gains inside CPF

You should leave your CPF OA untouched if:

- You plan to use the funds for housing in the next one to three years

- Your OA balance is below S$30,000 — the S$20,000 buffer leaves minimal investible savings

- You would be investing through high-fee unit trusts or ILPs where the fee alone eliminates the return advantage

- You have not yet built a cash investment portfolio — prioritise that first for the liquidity flexibility

- You are within 10 years of retirement and the guaranteed 2.5% p.a. suits your risk profile better than variable returns

What to Invest In (If You Decide to Invest)

If you have worked through the framework and investing makes sense for your situation, the product choice matters enormously. The CPFIS product list is broad — but most of it is not worth your time.

Avoid: High-cost unit trusts with expense ratios above 0.80% p.a. These are the products that have historically caused CPFIS investors to underperform the CPF OA’s 2.5% p.a. — the management fees consume the return advantage. Avoid ILPs (Investment-Linked Products) entirely — the cost structure is among the most opaque and expensive in the approved product list.

Consider: Low-cost index ETFs available under CPFIS-OA, such as the Nikko AM STI ETF (Singapore market) or the Lion-OCBC Securities HSBC Asia Pacific ex Japan Low Carbon ETF. These have expense ratios of 0.15–0.35% p.a. — low enough that the hurdle above 2.5% p.a. is realistic to clear over a 10+ year horizon.

Also consider: Endowus via CPFIS. Endowus is the only robo-advisor in Singapore that accepts CPF OA money and invests it into institutional-grade globally diversified funds with 100% trailer fee rebates. If you want managed, globally diversified exposure without selecting individual ETFs, Endowus on CPF OA is the cleanest route. The Endowus fee for CPF/SRS portfolios is 0.40% p.a. on top of underlying fund costs.

The OA-to-SA Transfer: The Often Better Alternative

Before investing your CPF OA, consider the alternative that does not involve any market risk at all: transferring OA to SA.

The SA currently earns 4% p.a. — guaranteed, risk-free, government-backed. That is 1.5 percentage points more than your OA. For S$20,000 transferred and held for 20 years, the compounding difference at 4% versus 2.5% is approximately S$13,000 in additional balance. No investment product offers that return guarantee.

The trade-off, stated plainly: the OA-to-SA transfer is irreversible. Transferred funds cannot be used for housing, cannot be withdrawn until retirement conditions are met, and cannot be reinvested in CPFIS-OA. If your life situation changes — unexpected housing need, career break, anything that requires CPF OA liquidity — you cannot undo the transfer.

For investors who are certain they do not need OA flexibility and want the guaranteed higher return without investment risk: the OA-to-SA transfer beats CPFIS-OA investing on a risk-adjusted basis at current rates. For investors who may need OA liquidity for any reason: keep the money in OA and do not transfer.

What IBKR, Webull, and Longbridge Have to Do With This

This is the nuance most CPF guides miss.

If you’re still unsure about CPF investments, you can start by investing spare cash instead. A good way to gain experience is through robo-advisors or brokerage accounts, which allow you to explore diversified portfolios and individual stocks.

IBKR, Webull, and Longbridge do not support CPFIS. None of the three brokers reviewed on DLCuration — Interactive Brokers, Webull Singapore, and Longbridge — are approved CPFIS agents. You cannot invest CPF OA money through any of them.

What they do provide is the optimal alternative: a cash investment portfolio that builds equity market experience and real returns without the CPF complexity. Before committing CPF OA to market risk, it makes sense to have demonstrated — through your own cash portfolio — that you can hold through a 20% correction without selling. A cash portfolio gives you that proof of concept. CPF OA should only follow once you have established your own investing discipline.

The recommended sequence for most Singapore investors:

Step 1: Leave CPF OA earning 2.5% p.a. (and consider the OA-to-SA transfer for any portion you are certain you will not need for housing)

Step 2: Build a cash investment portfolio via Webull, Longbridge, or IBKR — start with a globally diversified ETF and automate monthly contributions

Step 3: Once your cash portfolio has run for at least two to three years and you have experienced at least one meaningful market correction without selling, revisit the CPF OA investing question with the experience to answer it honestly

→ Start your cash investment portfolio with Webull → Open a Longbridge account for commission-free trading → Open an IBKR account for global market access

Frequently Asked Questions

What is the CPF OA interest rate in 2026?

The Ordinary Account interest rate remains at the floor rate of 2.5% per annum from 1 April to 30 June 2026. This rate is guaranteed and legislated — it cannot be reduced below 2.5% p.a. regardless of market conditions. The first S$20,000 in your OA earns an additional 1% extra interest, credited to your SA or RA rather than your OA.

How much CPF OA can I invest under CPFIS?

You can invest your OA savings after setting aside S$20,000 in your OA. Your investible savings is your OA balance plus any amounts previously withdrawn for investment and education, minus that S$20,000 floor. For stocks and ETFs listed under CPFIS, a further limit applies: you can only invest up to 35% and 10% of your investible savings in stocks and gold respectively.

Can I invest CPF OA through Webull, Longbridge, or IBKR?

No. These brokers are not approved CPFIS agent banks or CPFIS-approved brokerages. To invest CPF OA in stocks or ETFs, you need a CPFIS agent bank account (DBS/POSB, OCBC, or UOB) and a CPFIS-approved brokerage. Webull, Longbridge, and IBKR are suitable for cash investing only.

What happens if my CPF OA investments lose money?

You bear the loss. CPF Board does not compensate for investment losses under CPFIS. If your portfolio declines, your CPF OA balance upon selling is lower than if you had left the money earning 2.5% p.a. This is the core risk of CPFIS — and why the decision requires careful consideration of your time horizon and risk tolerance before proceeding.

Should I transfer CPF OA to SA instead of investing?

The OA-to-SA transfer earns a guaranteed 4% p.a. versus the OA’s 2.5% p.a. — a meaningful difference compounded over 10–20 years with zero risk. The major caveat is that this transfer is irreversible: transferred funds cannot be used for housing, cannot be withdrawn until retirement conditions are met, and cannot be reinvested in CPFIS-OA. If you are certain you will not need CPF OA liquidity for housing or other purposes, the OA-to-SA transfer often beats CPFIS-OA investing on a risk-adjusted basis at current CPF rates.

At what age does it stop making sense to invest CPF OA?

There is no hard age cutoff, but the general principle is that a shorter time horizon reduces the expected advantage of investing over the guaranteed 2.5% p.a. As you approach 50–55, the case for keeping CPF OA in the guaranteed account strengthens — particularly as the SA closure at age 55 means you will lose the 4% SA rate and the OA-to-SA transfer is no longer an option. CPF strategy becomes significantly more complex around age 55, and a licensed financial adviser familiar with CPF optimisation is worth consulting at that stage.

Final Thoughts

The CPF OA question does not have a universal right answer — and any article that pretends otherwise is either oversimplifying or selling you a product.

What this framework gives you is the honest set of considerations: a guaranteed 2.5% p.a. that most investment portfolios will fail to beat consistently after fees and behavioural costs, a set of specific conditions under which the case for investing is genuinely reasonable, and a clear sequence that most Singapore investors should follow (cash portfolio first, CPF OA later).

The most common mistake is investing CPF OA without a cash investment portfolio and without having experienced market volatility firsthand. The second most common mistake is leaving CPF OA uninvested for life out of inertia rather than deliberate choice.

Both are avoidable with a framework. Now you have one.

Reminder: CPF rules, rates, and eligibility criteria change. Verify all information at cpf.gov.sg before acting. Nothing in this article constitutes financial or investment advice. For personalised CPF strategy, consult a licensed financial adviser.

Where do you sit on the CPF OA investing debate — invested, transferred to SA, or keeping it in OA? Drop your reasoning in the comments; it is some of the most useful data a fellow Singapore investor can get.

Continue reading: